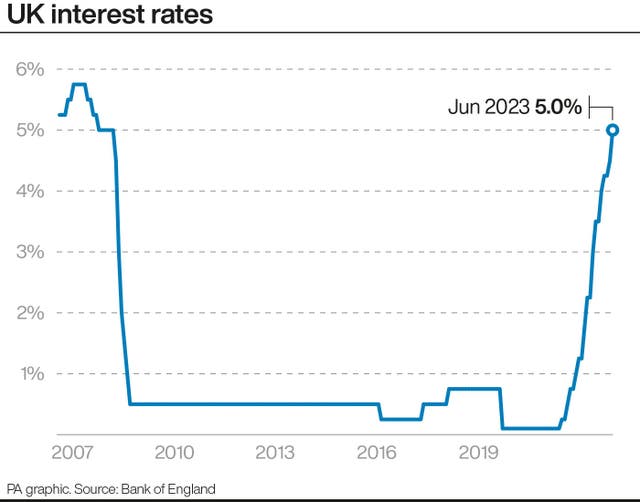

The Bank of England has unexpectedly pushed up interest rates to 5%, the highest rate in almost 15 years, as policymakers and the UK Government come under mounting pressure to control the cost-of-living crisis.

The move is set to deepen the mortgage crisis as borrowing costs are hiked up for the 13th time in a row.

The 0.5 percentage point increase was the sharpest increase since February, surprising economists who had been expecting a smaller hike of 0.25 percentage points.

Governor of the Bank of England Andrew Bailey said: “The economy is doing better than expected, but inflation is still too high and we’ve got to deal with it.

“We know this is hard – many people with mortgages or loans will be understandably worried about what this means for them.

“But if we don’t raise rates now, it could be worse later.”

It follows a higher-than-expected inflation reading in May as continued price rises forced policymakers into action in a bid to bring inflation down to the 2% target.

Calls are growing for the Government to do more to help mortgage borrowers who are set for a big jump in their monthly repayments.

Chancellor Jeremy Hunt said the Government’s resolve to bring inflation down was “watertight”.

He said: “The lesson from other countries is that if you stick to your guns, you bring inflation down.

“Our resolve to do this is watertight because it is the only long-term way to relieve pressure on families with mortgages. If we don’t act now, it will be worse later.”

Mr Hunt and Prime Minister Rishi Sunak have so far dismissed suggestions that ministers could intervene.

However, Mr Hunt is set to meet with lenders on Friday as pleas grow for more to be done and met with consumer champion Martin Lewis, who on Tuesday said that a mortgage ticking time bomb is now “exploding”.

Concerns over continued increases in wages alongside persistent goods and services inflation had already driven mortgage rates higher in recent weeks.

Financial markets have predicted that interest rates will strike a high of 6% by early next year amid warnings that 1.4 million mortgage holders will lose at least a fifth of their disposable income in additional repayments.

The central bank’s Monetary Policy Committee (MPC) said on Thursday that it made the decision to hike rates more sharply due to “the background of a tight labour market and continued resilience in demand”.

Seven members of the nine-person MPC opted for the increase to 5%, but two members called for rates to remain flat.

Why are you making commenting on The Herald only available to subscribers?

It should have been a safe space for informed debate, somewhere for readers to discuss issues around the biggest stories of the day, but all too often the below the line comments on most websites have become bogged down by off-topic discussions and abuse.

heraldscotland.com is tackling this problem by allowing only subscribers to comment.

We are doing this to improve the experience for our loyal readers and we believe it will reduce the ability of trolls and troublemakers, who occasionally find their way onto our site, to abuse our journalists and readers. We also hope it will help the comments section fulfil its promise as a part of Scotland's conversation with itself.

We are lucky at The Herald. We are read by an informed, educated readership who can add their knowledge and insights to our stories.

That is invaluable.

We are making the subscriber-only change to support our valued readers, who tell us they don't want the site cluttered up with irrelevant comments, untruths and abuse.

In the past, the journalist’s job was to collect and distribute information to the audience. Technology means that readers can shape a discussion. We look forward to hearing from you on heraldscotland.com

Comments & Moderation

Readers’ comments: You are personally liable for the content of any comments you upload to this website, so please act responsibly. We do not pre-moderate or monitor readers’ comments appearing on our websites, but we do post-moderate in response to complaints we receive or otherwise when a potential problem comes to our attention. You can make a complaint by using the ‘report this post’ link . We may then apply our discretion under the user terms to amend or delete comments.

Post moderation is undertaken full-time 9am-6pm on weekdays, and on a part-time basis outwith those hours.

Read the rules hereLast Updated:

Report this comment Cancel